Some Perspective On Year To Date Portfolio Declines

By: David M. Foster, CFP®, CAP®

All good things must come to an end, and the nearly uninterrupted upward march of US stocks from the lows of the COVID crisis appears to have done just that. How long this interruption lasts, we’ll have to wait and see, but in the meantime, I wanted to share some perspective on just what has occurred so far this year.

Year To Date Stock Market Performance

Remember how obvious it was in late March of 2020 that the stock market would more than double before the end of 2021?

Yea, me neither, but it happened anyway!

But, as you (hopefully) know already, the market doesn't always go straight up.

It's been a minute since we have experienced a decline like this, but, historically, this kind of thing happens quite regularly.

In an average year, the S&P 500 will fall by about 14% from it's calendar year high, which means that what we've experienced so far is pretty typical.

Of course, this time is different (because every time is different) because we are experiencing inflation the likes of which we haven't seen in 40ish years, and maybe there will be a nuclear war soon!

Understandably, "Consumer Sentiment" doesn't look so great.

But, as you can see from the chart above, troughs in consumer confidence have generally lead to excellent 12 month returns in the market. Of course, that doesn't mean it will this time, but it helps to keep in mind that consumer sentiment is mostly backward looking while the market (at least in theory) should be forward looking.

What about Bonds?

Ugh.

This is the worst start to the year for bonds since at least 1990, and by a wide margin.

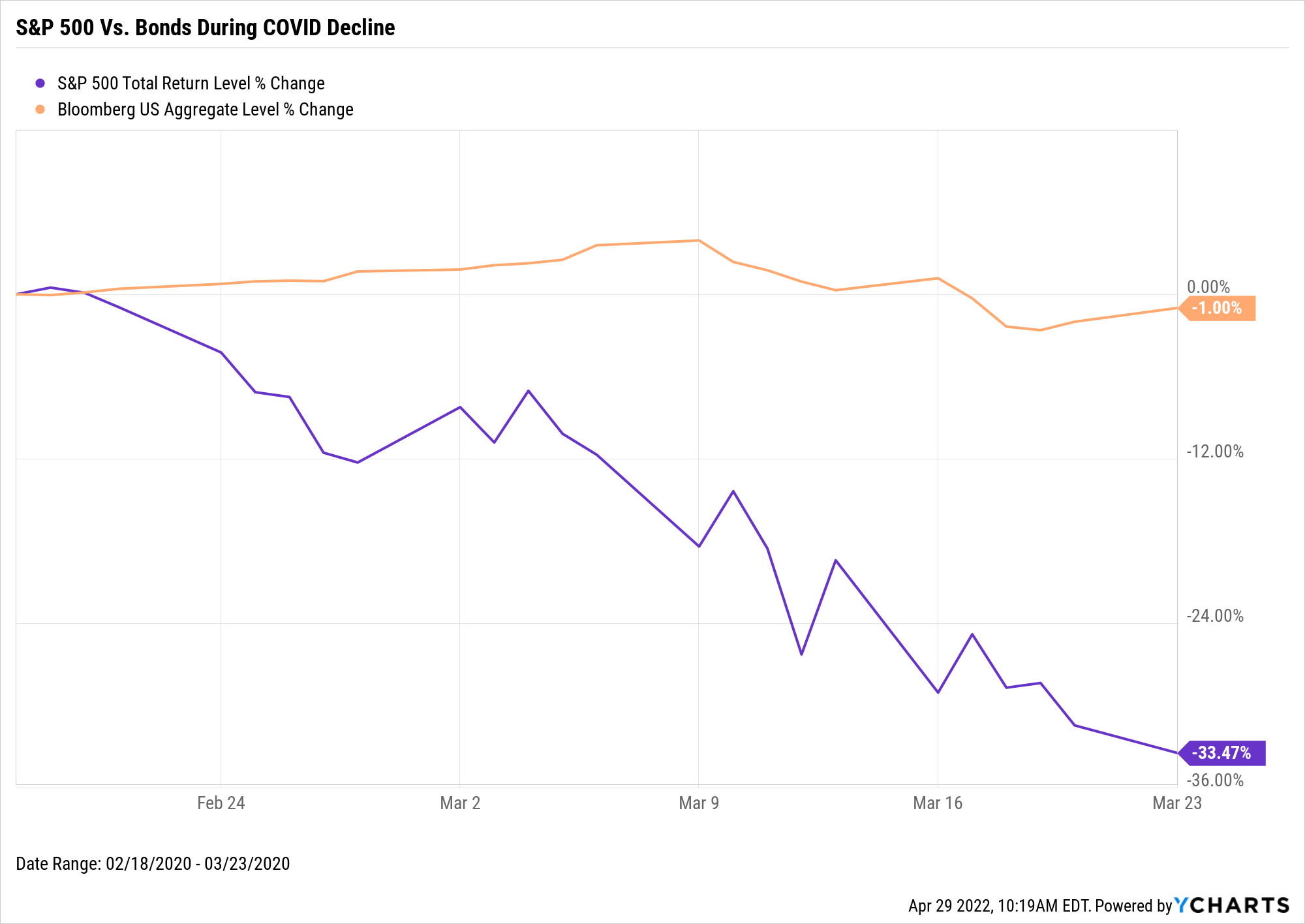

One of the primary reasons to own bonds, in addition to collecting fixed interest, is to give you something that will hold its value when stocks fall. Historically, that has looked something like this:

During that stretch right at the beginning of the pandemic, the S&P 500 fell by over a third and bonds were basically flat.

This year, on the other hand...

If you've been a client of mine for a while, you've probably heard me say that "A bad year for bonds is a bad day for stocks." Even with this year's decline, that's still true, as there have been roughly a dozen days when the market was down more in a single day (most recently in March of 2020) than bonds are over the last 12 months.

For the entirety of my 14 year career, the "experts" have been warning that rates had nowhere to go but up. Until recently, that prediction had been dead wrong. Of course, I have always known that something like this was a possibility, maybe even an inevitability. But, it still doesn't feel awesome now that it's come to pass.

However, here's the good news:

The reason that bonds have performed so poorly this year is because interest rates on those bonds are way, way up! A 2 Year Treasury that was previously paying about $80 on a $10,000 investment is now paying about $270, for a more than 3X increase!

Other than a brief interest rate spike in late 2018, these are the highest yields we've seen in about 14 years. In the short run, an increase in interest rates will cause existing bond prices to fall like they have this year, but, in the long run, the higher rates will be good for your bond holdings. This will be especially true if (and I know this is a big "if") we can get inflation under control in the relatively near future.

Putting It All Together

It's never fun to see your portfolio decline, especially when stocks aren't even down that much!

But, as is always the case, we have to keep a long term perspective.

$10,000 invested 20 years ago in the S&P 500 (you can't actually invest directly in an index, so this is hypothetical, although you can invest in index funds that can approximate one's return) would have grown to over $57,000, even after the recent drop!

And yes, bonds are down a bunch right now, but that makes them a much better deal today than they were a few months ago.

Obviously, if we could predict exactly when interest rates were going to change and by how much, or exactly when the stock market was going to peak and bottom, or exactly when a recession would begin and end, we would invest differently. We'd be jumping in and out stocks and bonds on a regular basis. But, until I can find someone to repair my crystal ball, as unsatisfying as it may feel at times, the best way to invest is to settle on a reasonable allocation between bonds, stocks, and cash based on your time horizon and income needs, and stick with it through good times and bad.

If you'd like to schedule a call to discuss how all of this affects you and your situation, please click here if you're an existing client, or click here if you're a prospective client.

Thanks for reading!

Hi, I'm David Foster! I wrote this blog post, and I am also the founder of Gateway Wealth Management, LLC. I hope you found something valuable in what you just read. If you'd like to read more about me, click here. If you'd like to read more about my firm, click here. Thank you for reading!

Contact

The information provided here is for general information only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. All indices are unmanaged and may not be invested into directly.

All investing involves risk including loss of principal. No strategy assures success or protects against loss. Past performance is no guarantee of future results.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The S&P 500 is an unmanaged index which cannot be invested into directly.